The euro’s moment

The euro has long been a powerful symbol of European unity and integration. Recent global developments have opened a window of opportunity to strengthen its role in the global financial system. In a world where fault lines are emerging in the United States’ (US) global appeal, the euro is gaining ground as a credible alternative. But Europe needs to act to foster a greater international role for the euro. Crucially, a savings and investments union and the digital euro are key to cement the euro’s role as a global financial anchor.

Fault lines are emerging in America’s global appeal

The narrative of US exceptionalism, anchored in macroeconomic outperformance and the dollar’s reserve currency status, has historically driven substantial global investments in US assets, including from Europe. But this year, US policy uncertainty, fiscal concerns, and stretched equity valuations led investors to start questioning that narrative. Investor concerns peaked when, following the 2 April US tariff announcement, traditional safe-haven assets like US Treasuries and the US dollar failed to provide meaningful diversification from US equity price declines. There were even days when all three declined simultaneously – a highly unusual pattern during periods of market stress.

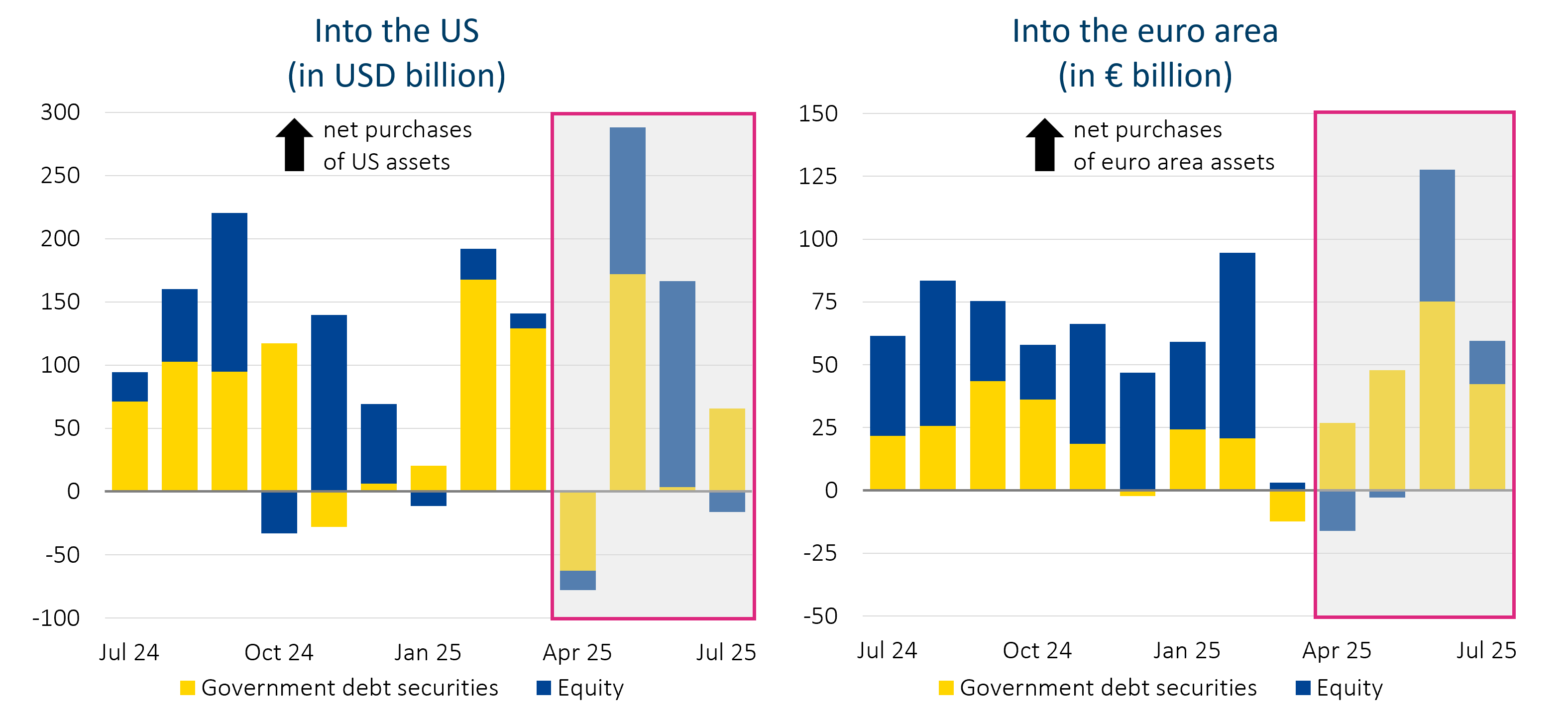

Indeed, April marked a clear ‘sell America’ moment, as foreign investors – mostly private – liquidated over USD 80 billion worth of US assets, reversing two years of continued inflows (Figure 1a). This moment proved to be temporary, as foreign demand came roaring back in May, more than offsetting April’s outflows.[1]

The continued US dollar weakness despite a rebound in capital flows into the US suggests that concerns about US policy and the safe-haven status of the dollar have not fully gone away. A new pattern has emerged, with investors increasingly hedging their US dollar exposures. And, while it is too soon to tell if changes in investor preferences are here to stay, some cracks in trust in the US dollar have emerged.

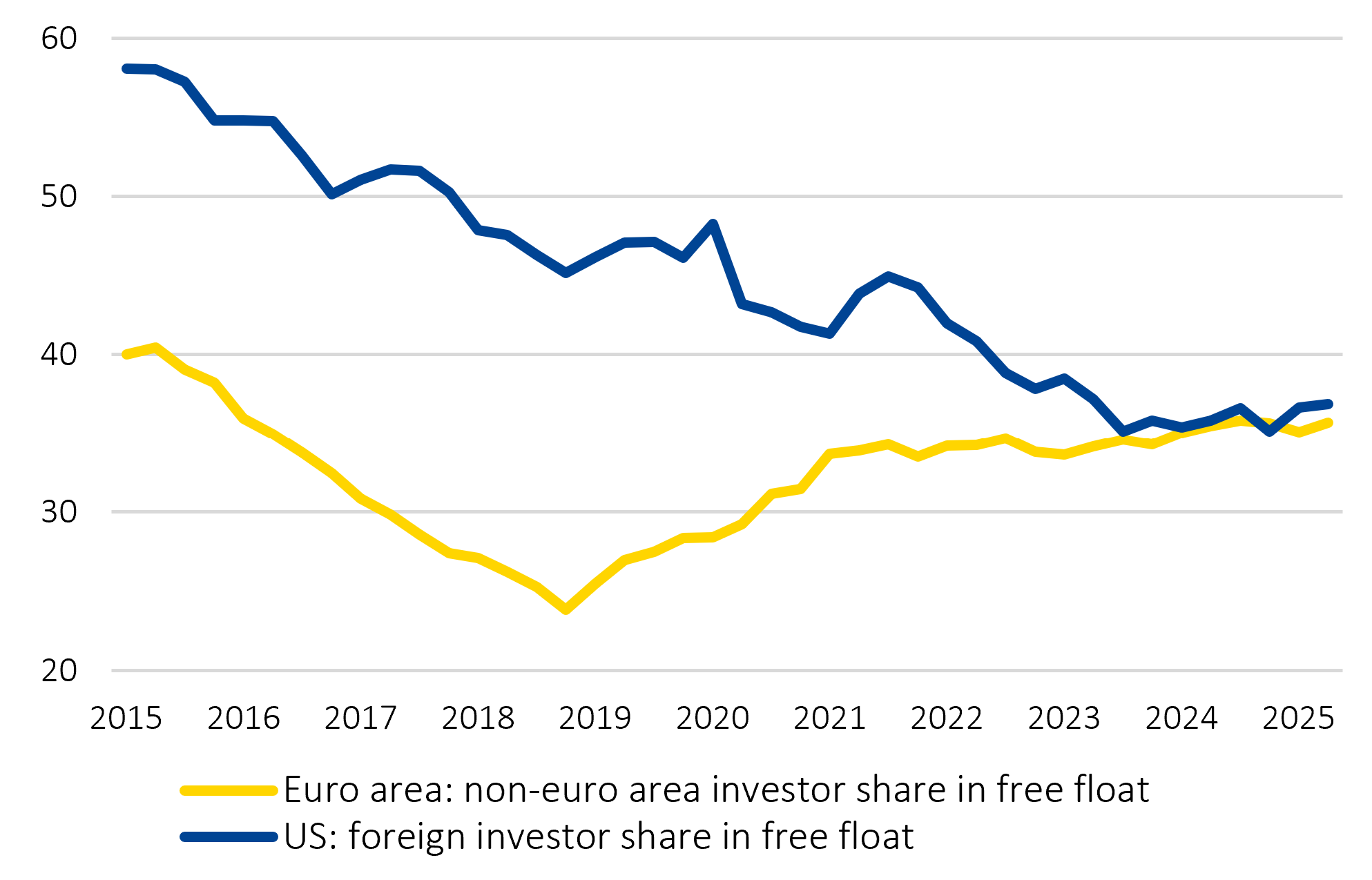

Figure 1: From recent inflows to longer-term trends, foreign demand underscores the euro’s growing appeal

1a: Monthly net purchases by foreign investors

Note: Transactions in government debt securities comprise both short-term and long-term securities, and for the US, includes both Treasuries and agencies bonds.

Source: ESM calculations based on data from the US Treasury International Capital system and the European Central Bank

1b: Foreign investors’ footprint

(% of sovereign marketable debt free float)

Notes: Up to Q2 2025. Sovereign marketable debt free float is defined, for the US, as Federal debt net of Federal Reserve holdings, and for the euro area, as government debt securities issued by 10 countries net of domestic government and Eurosystem holdings.

Source: ESM calculations based on European Central Bank and the US Department of the Treasury data.

An opportunity that Europe must grasp

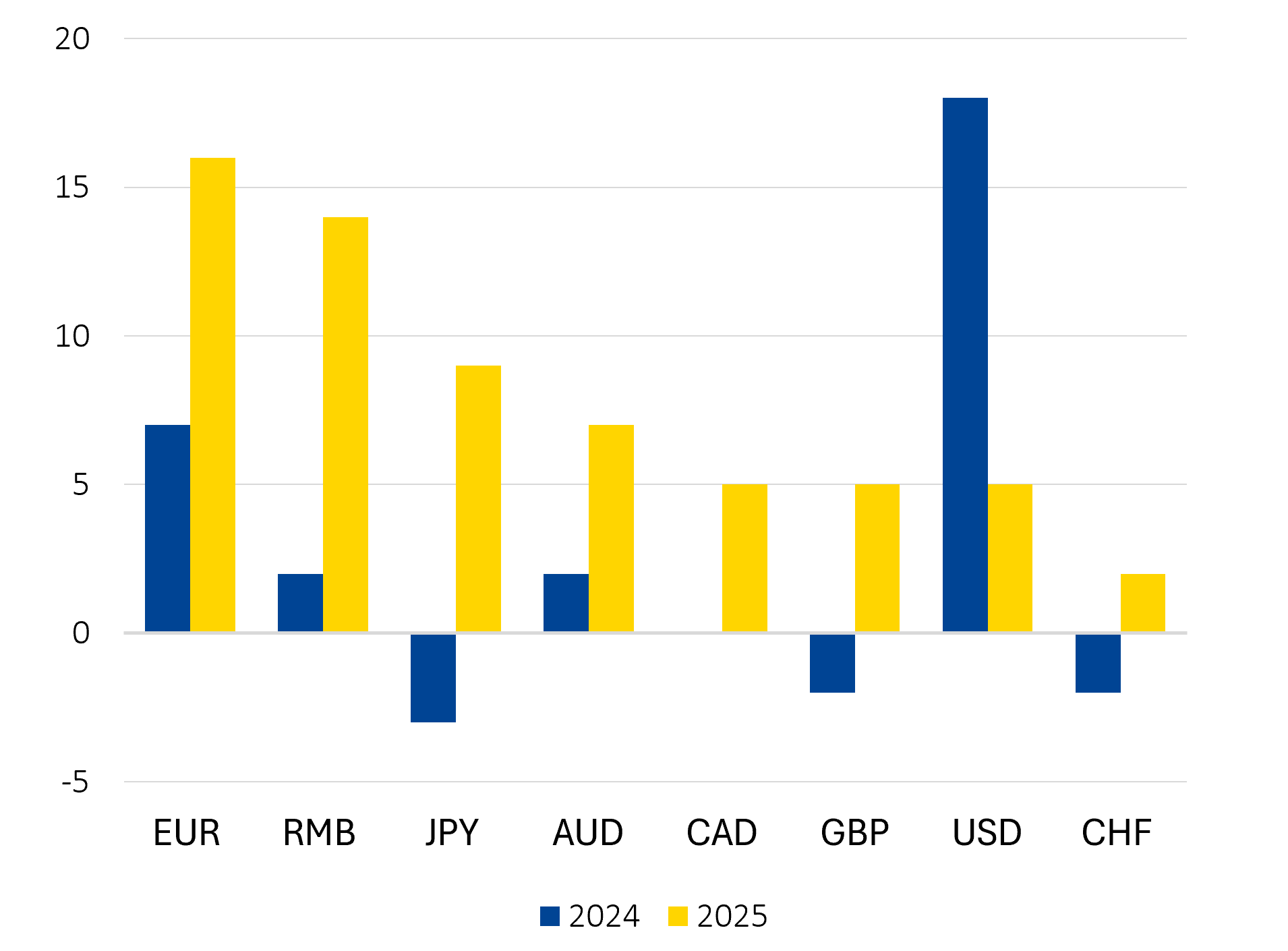

The euro is no doubt in demand: it has strengthened almost 14% against the US dollar so far this year.[2] Apart from flows related to increased hedging of exchange rate risk, some of this appreciation reflects a reallocation of investors’ portfolios in search of alternative safe havens and institutional stability. Just in the second quarter of 2025, foreign investors poured around €150 billion into euro area sovereign debt (Figure 1a) – the largest quarterly inflow since 2008 – with French, Italian, and Spanish bonds particularly in demand. Recent data shows that this momentum carried on into July. Euro-denominated issuance outside of the euro area has also expanded this year,[3] and, while dollar dominance as reserve currency is clear, recent surveys suggest central banks are increasingly planning to diversify their reserves towards the euro (Figure 2).[4]

Taking a longer-term perspective, the euro’s growing international appeal is also mirrored in a steady rise in foreign participation in euro area sovereign debt since 2019, while foreign holdings of US Treasuries were in downward trend (Figure 1b).

But more recent developments put Europe at a “strategic inflection point”, as European Central Bank (ECB) President Christine Lagarde framed it in her recent blog: the international monetary system might be moving towards a more multipolar regime, creating a unique opportunity for the euro to expand its global footprint. In this new emerging landscape, the euro can serve not only as a diversifier but also as a safe haven – supported by more predictable policy, stronger institutions, and a proven ability to manage crises.

Figure 2: A net 16% of surveyed central banks plan to raise their euro holdings — the highest for any currency

(net share of central banks surveyed anticipating increasing their currency exposure over the next 12-24 months, in %)

Source: Official Monetary and Financial Institution’s Forum’s Global Public Investor 2025 survey, OMFIF

A digital euro to cement the euro’s global role

A greater international role of the euro would be mirrored by increased capital inflows into Europe and a stronger currency. Sustained capital inflows could help fund Europe’s investment needs, reduce government borrowing costs by increasing demand, and enhance European strategic autonomy by reducing exposure to “dollarisation” of the world economy through US dollar-denominated stablecoins.

But to elevate the euro’s global standing, Europe urgently needs to act proactively on three key areas. Opportunities can easily turn into challenges if expectations are not met, and a lack of action will affect the euro’s relevance in the evolving global landscape.

First, Europe must deepen the Economic and Monetary Union. This includes further integration of the single market to boost long term growth and competitiveness. The Letta and Draghi reports’ recommendations[5] need to be acted upon. It also requires advancing the savings and investments union and expanding the supply of euro-denominated safe assets. This would strengthen Europe’s financial architecture, enhance risk sharing across the euro area, and improve the liquidity and attractiveness of euro-denominated assets.

Second, Europe must embrace innovation and urgently supplement the digital euro backed by the ECB as a safe public anchor, and support euro-denominated stablecoins under the Markets in Crypto-Assets (MiCA) Regulation. The Central Bank Digital Currency will facilitate payments, increase the euro’s usability in the evolving digital financial ecosystem and reduce reliance on US dollar-denominated stablecoins.

Third, Europe must embrace uncertainty and prepare itself to confront stablecoin issuance, for now largely denominated in US dollars. This means strengthening the MiCA regulation to avoid potential runs on pegs, shifting deposits affecting bank liquidity, and broad adoption affecting monetary policy effectiveness.

Finally, trust and stability remain essential but need to be earned. The credibility of the euro is built on the strength of the legal and institutional framework that supports it. Maintaining sound fiscal policies and ensuring financial stability, the core mandate of the ESM, are critical to reinforcing confidence in the euro.

Looking ahead

The euro has come a long way in its first quarter century. It has become a pillar of European integration, now supported by 5 out of 6 citizens in the euro area,[6] and a symbol of shared sovereignty. In a fragmenting world and an increasingly multipolar currency system, the euro can be an anchor of stability and enhance Europe’s strategic autonomy.

Strengthening the euro’s international role is desirable. The reforms highlighted above will require political will and strategic foresight. But the rewards are worth it.

Further reading

Lagarde, Christine. “Europe’s ‘global euro’ moment.” ECB Blog, 17 June 2025

Rehn, Olli. “Europe must not waste its currency moment.” VoxEU/CEPR blog, 11 July 2025

Acknowledgements

The author would like to thank Pilar Castrillo, Jemima Peppel-Srebrny, Alexandre Lauwers, Martin Rohár, Ashley Andrews, Andrzej Sowinski, and Cédric Crelo for their valuable suggestions and contributions to this blog post, as well as Raquel Calero for the editorial review.

Footnotes

About the ESM blog: The blog is a forum for the views of the European Stability Mechanism (ESM) staff and officials on economic, financial and policy issues of the day. The views expressed are those of the author(s) and do not necessarily represent the views of the ESM and its Board of Governors, Board of Directors or the Management Board.

Author

Blog manager